Estimated read time: 1-2 minutes

This archived news story is available only for your personal, non-commercial use. Information in the story may be outdated or superseded by additional information. Reading or replaying the story in its archived form does not constitute a republication of the story.

SALT LAKE CITY — If you own your home, it's not just about keeping up with repairs. You'll also want to keep up with your credit.

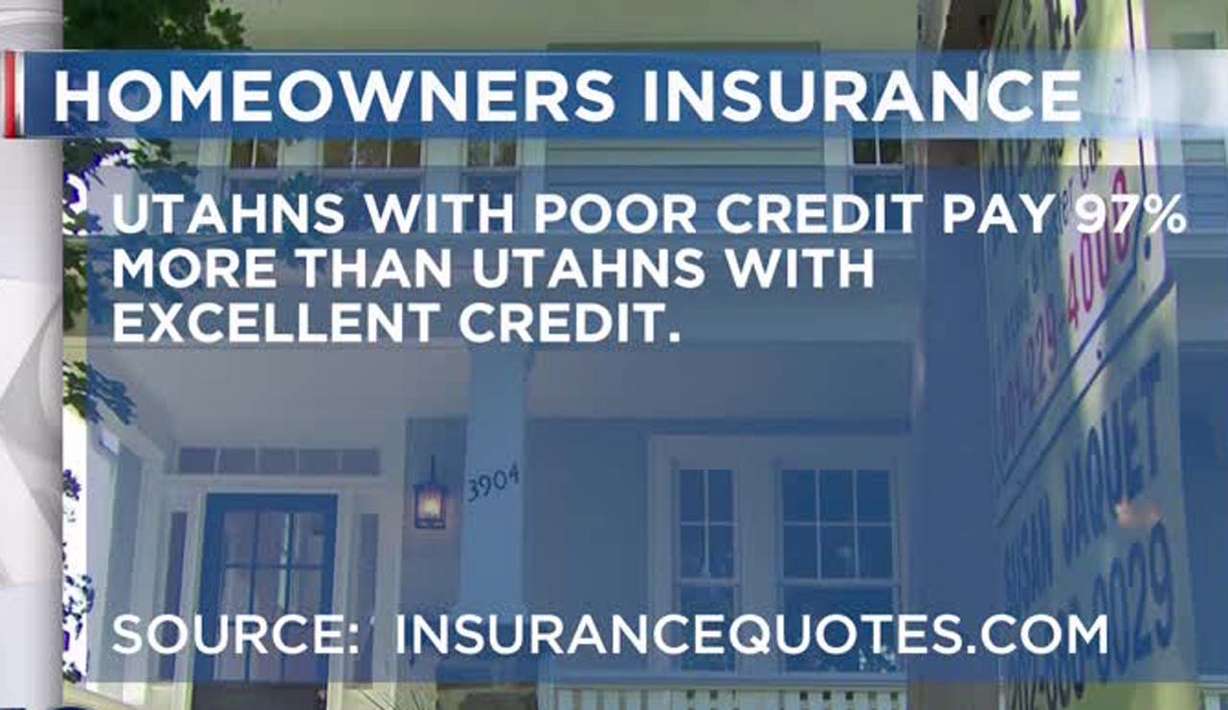

A recent study by InsuranceQuotes.com finds Utahns with poor credit pay 97 percent more — nearly twice as much — for homeowners insurance than people with excellent credit.

Once KSL Investigators heard that figure, we contacted Laura Adams, a senior data analyst for the company.

"I think a lot of consumers are very unaware of the role credit plays in our insurance life," Adams said.

She says insurance companies have found a very strong statistical link between consumers with poor credit and the filing of more claims.

"For insurance companies, it's all about how risky you are to them," she said. "Consumers with poor credit are riskier."

Independent insurance broker Dave Platt is not convinced Utah homeowners with poor credit pay twice as much for their insurance.

"Absolutely, it's a big factor, some companies use it quite a bit, and rely on it very heavily," he said.

Platt went on to say that claims will probably have a bigger impact than credit score.

He says Utah insurers use formulas factoring in parts of our credit histories that can predict how likely we are to file claims in the future.

"If you're late on medical bills, it's of no significance on whether or not you file future insurance claims, so most insurance companies throw that right out," he said.

"Where if you're chronically behind on paying your utility bills or mortgage payment, that really is a good predictor that you're going to file more insurance claims," he added.

- By shopping around you can find lower rates even if your credit score is low.

- Combine your auto and home insurance with the same insurer.

- Platt suggests using home insurance for the big things you cannot afford to pay out of your pocket such as fire damage. Filing smaller claims can lead to higher rates.