- Utah drivers face rising car insurance costs due to various factors.

- Shopping around can save up to $4,700 annually between insurers.

- Factors like marital status, mileage and violations significantly impact rates.

SALT LAKE CITY — Utah drivers are getting squeezed by car insurance, but new data shared with KSL shows there are some very specific things drivers may be doing that are pushing their bills higher.

Think of it as a cheat sheet for your car insurance bill. Some of it you can control. Some of it you cannot. But the numbers are big enough that it is worth knowing what is moving your rate.

Missed savings

Start with the big one: shopping around.

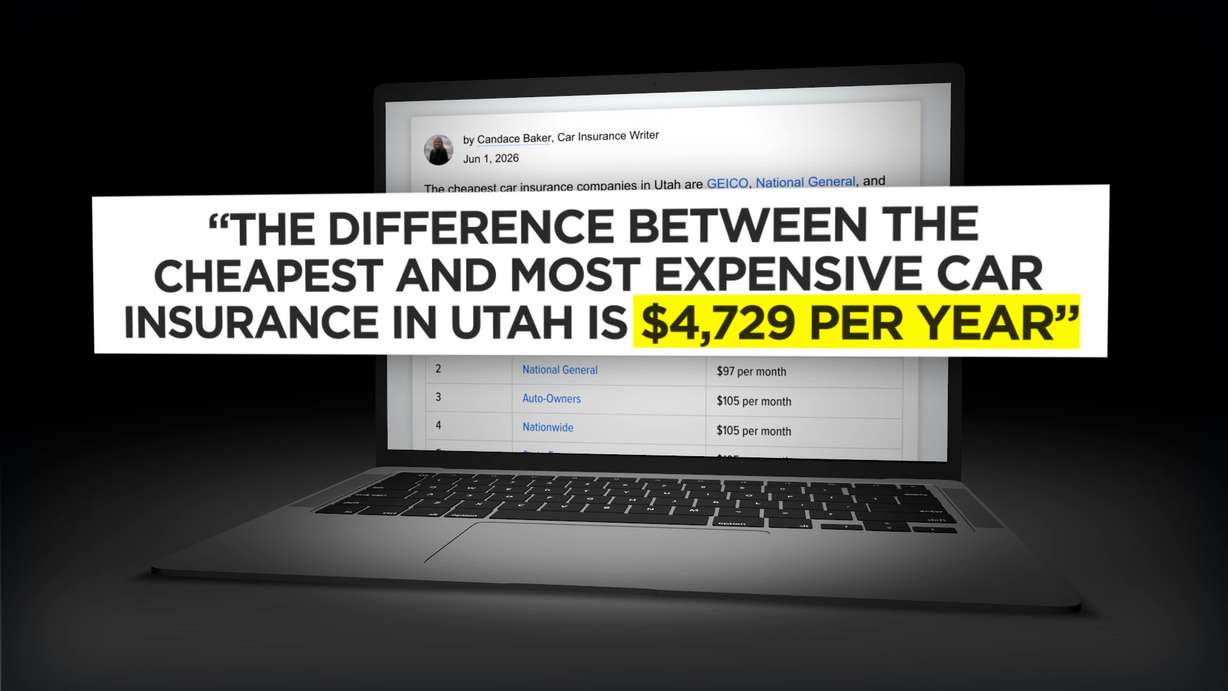

A new analysis from WalletHub found the difference between Utah's cheapest and most expensive car insurance companies is more than $4,700 a year.

"It's a huge margin," said Chip Lupo, WalletHub writer and analyst.

Lupo said cheaper is not always better. Drivers should also compare coverage, deductibles and customer service. But with prices that differ so drastically, it is worth asking questions before automatically renewing the same policy.

"Too many people get comfortable with their current policy and just automatically renew every year, even if the rates go up without any real understanding why they would go up," Lupo said.

So, what else can affect the price?

WalletHub's analysis found married drivers pay about 5% less than single drivers. Keeping continuous insurance coverage matters, too. Utah drivers who allow their insurance to lapse pay about 7% more.

Mileage can also make a difference, especially as more people work from home or follow hybrid schedules.

Driving 7,500 miles a year instead of 20,000 can mean paying about 6% less.

But the savings only happen if the insurance company knows a driver's habits have changed.

"It's on the individual policyholder to keep the insurance company aware of any changes," Lupo said.

Costly mistakes

Then there are the expensive mistakes behind the wheel.

According to the analysis, a speeding ticket can increase a Utah driver's rate by 24%.

A red-light violation can also mean a 24% increase.

An at-fault accident or open-container violation can increase rates by about 50%.

Reckless driving or a DUI can push rates up 129%, while a suspended license can mean paying 137% more.

Factors out of your control

Other factors are not so easy to change.

Age is a major one. The analysis found 16-year-old drivers pay 420% more than 55-year-old drivers.

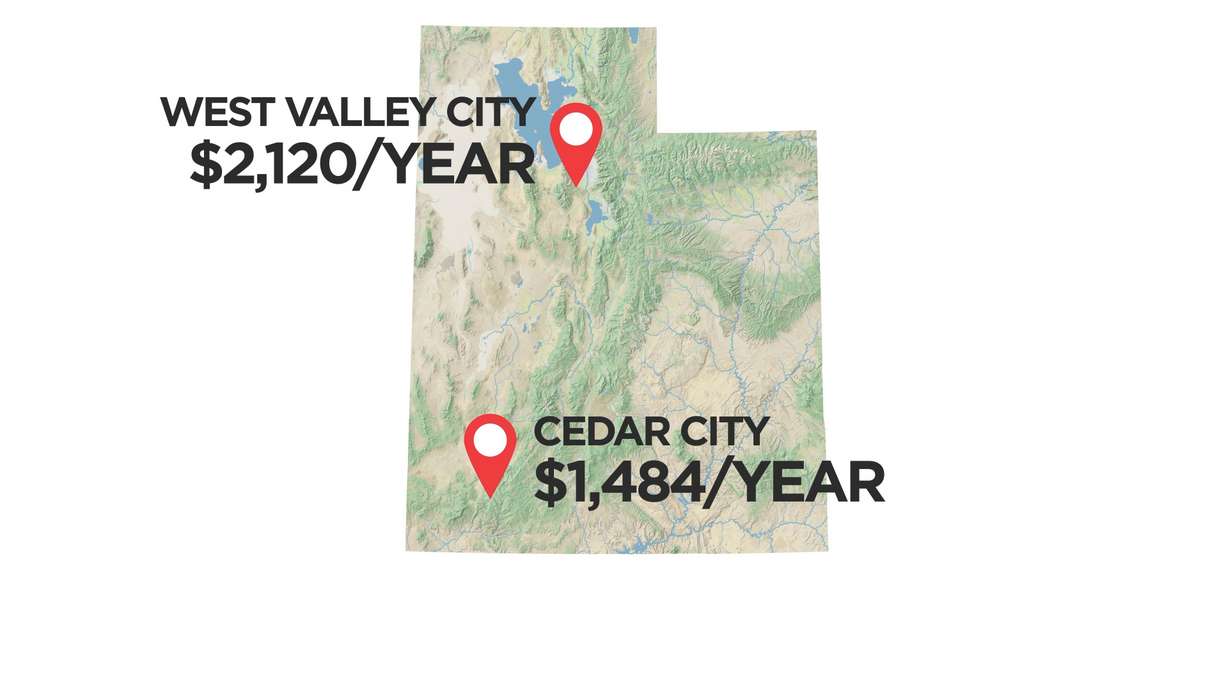

Where a driver lives also matters. Drivers in Cedar City paid an average of $1,484 a year, according to WalletHub. Drivers in West Valley City paid an average of $2,120, nearly 43% more.

Moving from West Valley City to Cedar City may not be a realistic option, but before renewing a policy, drivers can call their agent and ask a few questions:

Can I get a better quote?

Am I missing any discounts?

Does my coverage still match my life?

Drivers should then call a couple of other agents or insurance companies to compare. The savings could be stark.