'%3e%3cpath%20d='M34.1406%205.85938C30.3906%202.10547%2025.3047%200%2020%200C14.6953%200%209.60938%202.10547%205.85938%205.85938C2.10938%209.61328%200%2014.6953%200%2020C0%2025.3047%202.10547%2030.3906%205.85938%2034.1406C9.61328%2037.8906%2014.6953%2040%2020%2040C25.3047%2040%2030.3906%2037.8945%2034.1406%2034.1406C37.8906%2030.3906%2040%2025.3047%2040%2020C40%2014.6953%2037.8945%209.60938%2034.1406%205.85938ZM37.0117%2023.543H31.1602V13.5391H27.6328V19.9414C28.1211%2020.6914%2028.3711%2021.582%2028.3711%2022.5625V22.625C28.3711%2023.668%2028.1172%2024.6055%2027.6328%2025.4297V26.6094H36.082C33.4883%2032.9375%2027.2891%2037.3789%2020.0039%2037.3789C10.3711%2037.3789%202.62109%2029.6289%202.62109%2020C2.62109%2010.3711%2010.3711%202.62109%2020%202.62109C29.6289%202.62109%2037.3789%2010.3711%2037.3789%2020C37.3789%2021.1484%2037.2617%2022.2656%2037.0508%2023.3477C37.0391%2023.4141%2037.0234%2023.4766%2037.0117%2023.543Z'%20fill='white'/%3e%3cpath%20d='M22.3086%2018.5352C20.4336%2018.125%2019.9531%2017.8398%2019.9766%2017.1836V17.1406C19.9766%2016.6992%2020.3477%2016.2148%2021.4023%2016.2148C22.582%2016.2148%2023.8867%2016.6797%2025.0781%2017.4766L26.8516%2015.0195C25.4453%2013.8906%2023.707%2013.3398%2021.5547%2013.3398C18.5195%2013.3398%2016.4375%2015%2016.4063%2017.4766V17.5352C16.3633%2020.2617%2018.5859%2020.9805%2021.293%2021.6016C23.0391%2021.9766%2023.5703%2022.3164%2023.5703%2022.9609L23.5469%2022.9766C23.5469%2023.3906%2023.2578%2023.7031%2022.7852%2023.8359C22.5742%2023.9062%2022.1289%2023.9727%2021.5156%2023.9727C20.7617%2023.9727%2019.7539%2023.8633%2018.6328%2023.4844C18.0898%2023.2891%2017.4727%2023.0039%2016.8047%2022.6133L20.1406%2026.625C20.2813%2026.6602%2021.0977%2026.8516%2021.7734%2026.8516C25.0039%2026.8516%2027.0859%2025.2461%2027.1094%2022.6328V22.5703C27.1602%2020.1133%2025.2148%2019.1719%2022.3086%2018.5352Z'%20fill='white'/%3e%3cpath%20d='M5.24219%2013.5664V26.6133H8.75391V23.7578L10.2969%2021.9531L14.2031%2026.6133H18.3867L12.3555%2019.5195L17.4023%2013.5664H13.4531L8.75391%2019.0586V13.5664H5.24219Z'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_97_2430'%3e%3crect%20width='40'%20height='40'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Estimated read time: 3-4 minutes

This archived news story is available only for your personal, non-commercial use. Information in the story may be outdated or superseded by additional information. Reading or replaying the story in its archived form does not constitute a republication of the story.

SALT LAKE CITY — Buy-now-pay-later plans don't sound like a particularly fresh consumer idea, and the emerging digital take on once ubiquitous layaway plans are really just app-based reboots, but it's a payment choice that can lead to harsh consequences for the unwary.

A growing number of tech platforms, that include programs from Affirm, Afterpay, Klarna, Sezzle and Zip, are finding success in partnering with retailers to offer portals for issuing credit at time of purchase that allows the consumer to check out, virtually or in person, with their goodies after agreeing to an installment plan. Some charge interest, some don't, and rescheduling a payment or paying late can also come with charges.

And perhaps the most significant consequence is how easy buy-now-pay-later plans make it to overextend via what is essentially a loan application process that takes only moments to complete.

Buy-now-pay-later providers have carved out a consumer financing niche, using real-time "soft" credit inquiries that don't pull up credit scores, don't appear on the applicant's credit report and, should credit be issued, doesn't report new debt obligations back to credit agencies. This opens the door for applicants who may not qualify based on their scores, want to avoid maxing out current credit cards or who simply don't have ample credit history to pass a more in-depth credit assessment.

No-fees, sort of: For many of the new buy-now-pay-later systems, their no-interest or no-fee marketing promises hold up, but only as long as you adhere to the contract-stipulated installment plan.

If you miss a payment, many of the apps have late fees that kick in while others apply interest rates reaching as high as 30%, per a report released earlier this year by U.S. PIRG. Missing payments may cause buy-now-pay-later debt to be turned over to debt collectors, or end up as dings on a consumer's credit report. These repercussions are not uncommon in the buy-now-pay-later world; more than seven out of 10 customers have faced late fees or interest rate charges. According to one study, 72% of those who had fallen behind on payments saw their credit score fall as a result.

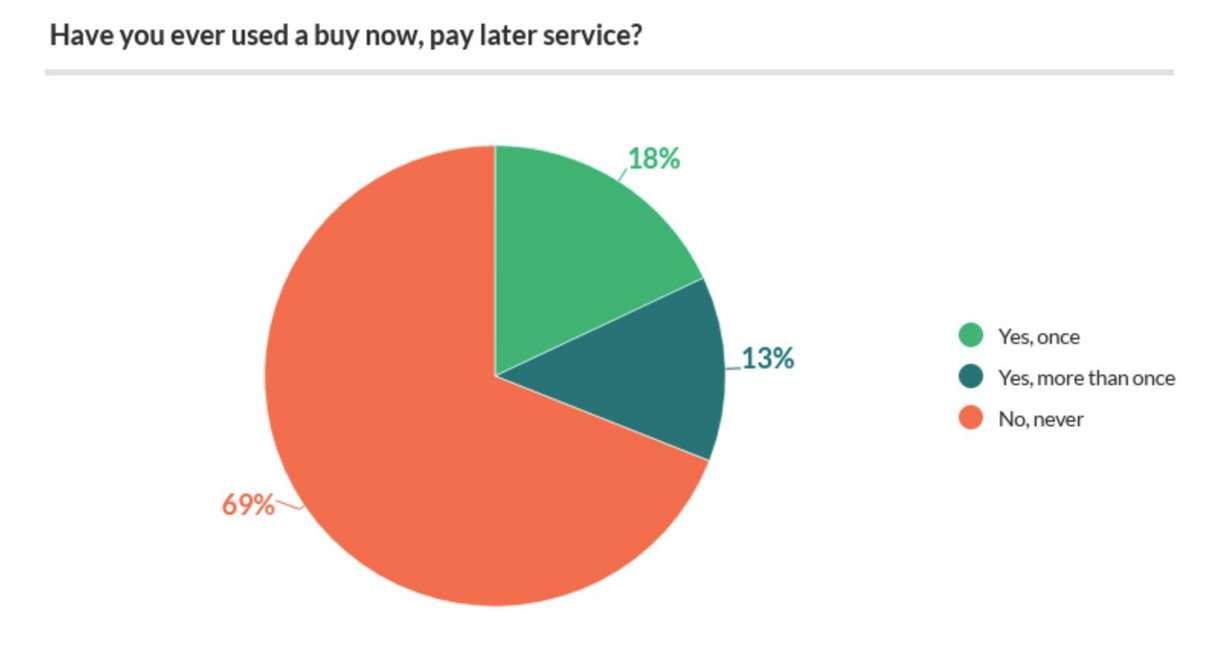

Too easy?CNBC reports nearly 45% of shoppers have now signed up for at least one buy-now-pay-later plan, according to a survey by DebtHammer.org — a 41% jump since April of last year.

Of those who've used the installment payment plans, 22% regret their decision, the report found.

And, roughly 30% said they've struggled to keep up with the payments and have had to skip paying an essential bill to avoid defaulting, per CNBC.

Separate studies have also shown that installment buying could encourage consumers to spend more than they can afford on impulse purchases.

"People are buying 'wants' not 'needs,'" Howard Dvorkin, CPA and chairperson of Debt.com, told CNBC.

New regulatory scrutiny: The Consumer Financial Protection Bureau opened an inquiry late last year into popular buy now, pay later programs Afterpay, Affirm, Klarna, PayPal and Zip, according to CNBC.

The financial watchdog said it is particularly concerned about how these programs impact consumer debt accumulation, as well as what consumer protection laws apply and how the payment providers harvest data.

"Buy now, pay later is the new version of the old layaway plan, but with modern, faster twists where the consumer gets the product immediately but gets the debt immediately, too," CFPB Director Rohit Chopra said in a statement to CNBC.